Moirai-R models

Collection

10 items • Updated • 46

Moirai, the Masked Encoder-based Universal Time Series Forecasting Transformer is a Large Time Series Model pre-trained on LOTSA data. For more details on the Moirai architecture, training, and results, please refer to the paper.

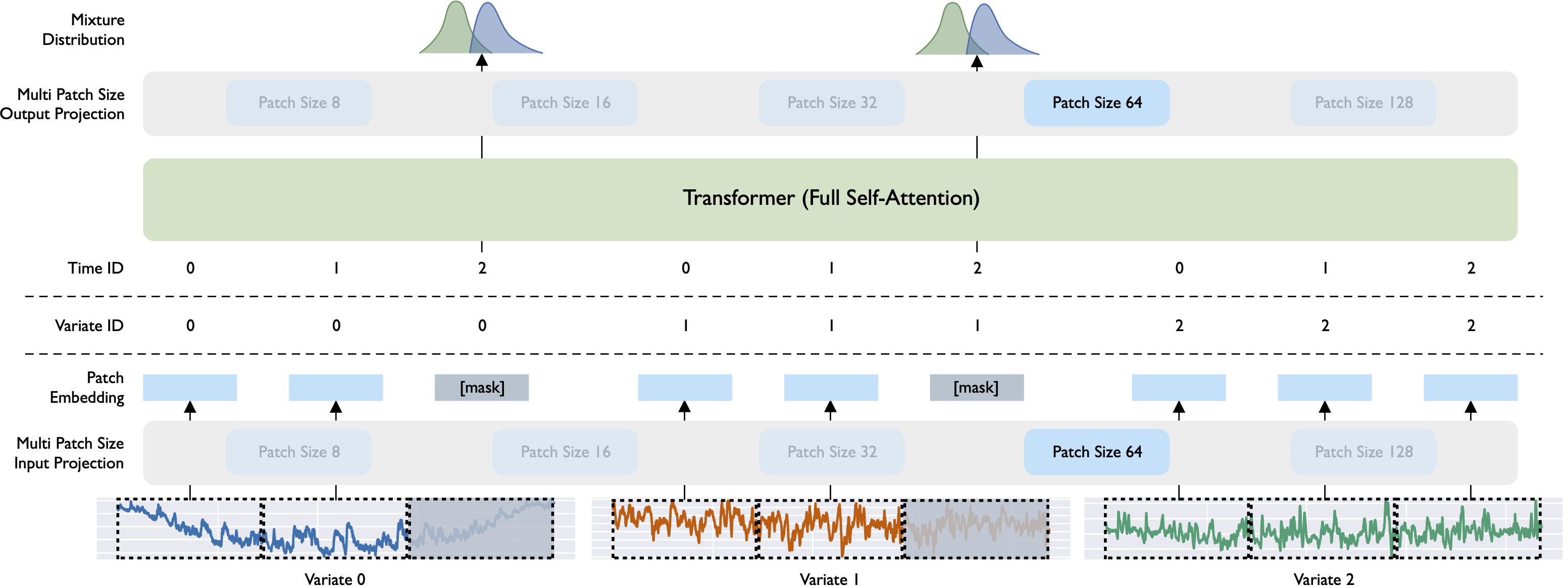

Fig. 1: Overall architecture of Moirai. Visualized is a 3-variate time series, where variates 0 and 1 are target variables (i.e. to be forecasted, and variate 2 is a dynamic covariate (values in forecast horizon known). Based on a patch size of 64, each variate is patchified into 3 tokens. The patch embeddings along with sequence and variate id are fed into the Transformer. The shaded patches represent the forecast horizon to be forecasted, whose corresponding output representations are mapped into the mixture distribution parameters.

To perform inference with Moirai, install the uni2ts library from our GitHub repo.

git clone https://github.com/SalesforceAIResearch/uni2ts.git

cd uni2ts

virtualenv venv

. venv/bin/activate

pip install -e '.[notebook]'

.env file:touch .env

A simple example to get started:

import torch

import matplotlib.pyplot as plt

import pandas as pd

from gluonts.dataset.pandas import PandasDataset

from gluonts.dataset.split import split

from uni2ts.eval_util.plot import plot_single

from uni2ts.model.moirai import MoiraiForecast, MoiraiModule

SIZE = "small" # model size: choose from {'small', 'base', 'large'}

PDT = 20 # prediction length: any positive integer

CTX = 200 # context length: any positive integer

PSZ = "auto" # patch size: choose from {"auto", 8, 16, 32, 64, 128}

BSZ = 32 # batch size: any positive integer

TEST = 100 # test set length: any positive integer

# Read data into pandas DataFrame

url = (

"https://gist.githubusercontent.com/rsnirwan/c8c8654a98350fadd229b00167174ec4"

"/raw/a42101c7786d4bc7695228a0f2c8cea41340e18f/ts_wide.csv"

)

df = pd.read_csv(url, index_col=0, parse_dates=True)

# Convert into GluonTS dataset

ds = PandasDataset(dict(df))

# Split into train/test set

train, test_template = split(

ds, offset=-TEST

) # assign last TEST time steps as test set

# Construct rolling window evaluation

test_data = test_template.generate_instances(

prediction_length=PDT, # number of time steps for each prediction

windows=TEST // PDT, # number of windows in rolling window evaluation

distance=PDT, # number of time steps between each window - distance=PDT for non-overlapping windows

)

# Prepare pre-trained model by downloading model weights from huggingface hub

model = MoiraiForecast(

module=MoiraiModule.from_pretrained(f"Salesforce/moirai-1.0-R-{SIZE}"),

prediction_length=PDT,

context_length=CTX,

patch_size=PSZ,

num_samples=100,

target_dim=1,

feat_dynamic_real_dim=ds.num_feat_dynamic_real,

past_feat_dynamic_real_dim=ds.num_past_feat_dynamic_real,

)

predictor = model.create_predictor(batch_size=BSZ)

forecasts = predictor.predict(test_data.input)

input_it = iter(test_data.input)

label_it = iter(test_data.label)

forecast_it = iter(forecasts)

inp = next(input_it)

label = next(label_it)

forecast = next(forecast_it)

plot_single(

inp,

label,

forecast,

context_length=200,

name="pred",

show_label=True,

)

plt.show()

| # Model | # Parameters |

|---|---|

| Moirai-1.0-R-Small | 14m |

| Moirai-1.0-R-Base | 91m |

| Moirai-1.0-R-Large | 311m |

If you're using Uni2TS in your research or applications, please cite it using this BibTeX:

@article{woo2024unified,

title={Unified Training of Universal Time Series Forecasting Transformers},

author={Woo, Gerald and Liu, Chenghao and Kumar, Akshat and Xiong, Caiming and Savarese, Silvio and Sahoo, Doyen},

journal={arXiv preprint arXiv:2402.02592},

year={2024}

}

This release is for research purposes only in support of an academic paper. Our models, datasets, and code are not specifically designed or evaluated for all downstream purposes. We strongly recommend users evaluate and address potential concerns related to accuracy, safety, and fairness before deploying this model. We encourage users to consider the common limitations of AI, comply with applicable laws, and leverage best practices when selecting use cases, particularly for high-risk scenarios where errors or misuse could significantly impact people’s lives, rights, or safety. For further guidance on use cases, refer to our AUP and AI AUP.